This article is an excerpt from the InvestorPlace Digest newsletter. To get news like this delivered straight to your inbox, click here.

It’s been a rough month for high-growth tech stocks. The tech-heavy Nasdaq-100 index has fallen 6% since July, and many of its constituents are down even more. Fast-growing moonshots from Enphase Energy (NASDAQ:ENPH) to electric vehicle maker Tesla (NASDAQ:TSLA) have lost close to 20% of their market values in less than a month.

That’s because investors have been pivoting into safer stocks. Over the past month, some of the top performers have included pharma company Eli Lilly (NYSE:LLY) (up 20%), energy company APA (NASDAQ:APA) (up 16%), and telecom firm Charter Communications (NASDAQ:CHTR) (up 9%).

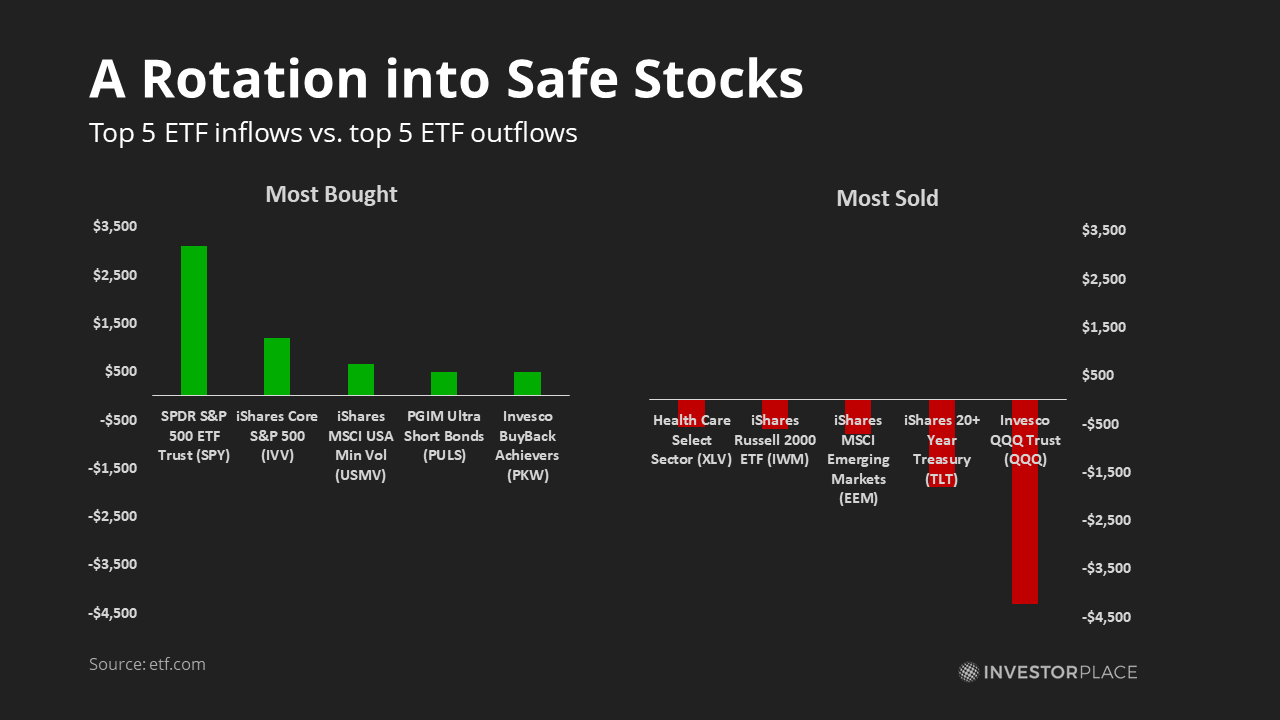

These moves are reflected in fund flow data.

In the past week alone, investors have unloaded $4.2 billion of the popular Nasdaq-100 ETF Invesco QQQ Trust (NASDAQ:QQQ), making it the most sold exchange-traded fund in the world.

Meanwhile, blue-chip ETFs are gaining ground. During the same period, ETF inflows went into S&P 500 indices and the iShares MSCI USA Min Vol ETF (BATS:USMV) – an index tracker that seeks to reduce volatility.

Our writers at InvestorPlace.com, our free news site, have also pivoted to recommending shares of safer stocks, especially firms that will thrive in a market pullback.

With investor sentiment suddenly taking a downwards turn, here are the five under-$40 safe stocks our writers and analysts are recommending this week…

5 Safe Stocks Under $40 to Buy Immediately: Pfizer (PFE)

Shares of Pfizer (NYSE:PFE) fell 30% this year as investors pivoted away from the Covid-19 winner. Prices of the pharma giant now sit below their pre-pandemic levels

InvestorPlace.com writer Jeremy Flint sees this as a perfect opportunity to buy in.

Here’s from his recent update:

Pfizer remains focused on the future, with a robust pipeline ensuring a steady stream of revenue. Its production and distribution networks also ensure the company can compete against generics, threatening its bottom line. Analysts are just as bullish on Pfizer, with estimates indicating PFE is nearly 35% undervalued today. The company’s growing revenue, profits, and 4% dividend yield also make Pfizer perfect for undervalued blue-chip seekers.

Essentially, bearish investors have become overly focused on Pfizer’s declining sales of Comirnaty and Paxlovid – two Covid-19 treatments with plummeting demand. To these skeptics, Pfizer has become the next Gilead Sciences (NASDAQ:GILD) – a company that became reliant on therapies for a single disease. It’s a high-risk strategy that can quickly fall apart once that disease ebbs. (Gilead still trades 32% below its 2015 high).

But Pfizer is no one-trick pony. The New York-based company has dozens of other high-performing treatments on the market, and owns a pipeline with several potential blockbusters in the making. Its treatments for respiratory disease, migraines, and blood cancers could be worth $1 billion or more.

Pfizer’s size also gives it significant advantages in the pharma industry. According to data from Thomson Reuters, the company outspends all but two competitors in research and development (R&D). Its sales team is also one of the most efficient in the industry, with overheads consuming less than 17% of the company’s revenues.

That makes Pfizer’s $35 stock an unusual outlier in its industry. Shares currently trade at 10X forward earnings, a level that probably won’t last long.

2. Intel (INTC)

Many investors mistakenly view Intel (NASDAQ:INTC) as a risky turnaround. The company’s failure to keep up with Taiwan Semiconductor Manufacturing (NYSE:TSM) has left the Silicon Valley pioneer a generation behind in chip technology. Intel’s R&D bosses are now trying to leapfrog to 1.8-nanometer technology, a risky strategy that might not pay off.

Yet, Intel remains the dominant player in CPU and server chips.

The company has increased its share of the CPU market by 6.4% to 82.7% this year and has been aggressively defending its server business from Advanced Micro Devices (NASDAQ:AMD).

Analysts expect Intel to generate $20 billion in operating cash in 2024, a 32% increase from last year’s figures.

This week, Larry Ramer from InvestorPlace.com joins top analyst Eric Fry and me in recommending Intel, a company that Eric calls “the next trillion-dollar stock.”

Intel looks poised to get strong boosts from multiple, powerful trends. Specifically, the company is well-positioned to be lifted by the increased demand for PCs and by its AI chips…

The company is also building a large semiconductor factory in Arizona, and will get subsidies for its chip factories from Washington and the EU. Further, Nvidia has expressed interest in having Intel build its chips.

Intel is far safer of a stock than people realize.

Artificial intelligence servers still require powerful CPUs that Intel produces. And even Intel’s higher-cost fabrication business will soon become an asset. Governments are waking up to the risks of outsourcing advanced chipmaking and are pouring taxpayer money into homegrown players. Even Nvidia (NASDAQ:NVDA) might use Intel to produce its chips someday.

Eric just released a presentation on how the stage is set for AI once again. Only this time, we’re on the verge of seeing an AI panic unlike anything you could ever imagine. Watch Eric share his 1,000% AI blueprint for turning the coming panic into 1,000% profit potential in the days ahead.

3. SoFi Technologies (SOFI)

Shares of SoFi Technologies (NASDAQ:SOFI) have pulled back in recent weeks, despite the firm announcing a “beat-and-raise” quarter. Q2 earnings came in well ahead of expectations, and the fintech firm raised its full-year 2023 revenue guidance to $2 billion of adjusted net revenue.

It’s why top InvestorPlace.com analyst Louis Navellier and his team now sees SoFi’s $8 share price a golden opportunity to buy in. They note that the “neobank” likely remains on track to achieve GAAP profitability by Q4.

To see more about Louis’ most recent presentation, click here.

“Although it is far from certain how this stock will perform in the near-term as the long-term growth potential of this financial services industry disruptor remains intact, the chances of higher prices for shares down the road remain very strong.”

Fundamentally, SoFi is a financial institution that uses student loans as a loss leader to access potential customers. Shares sold off in 2022 as investors wondered whether the company could convert enough borrowers into higher-margin products to survive.

This year’s results have shown the answer is “yes.” On July 31, SoFi revealed the number of checking and savings customers rose 47% year over year, vastly outpacing the 6% growth in student loans. Rising interest rates would further push SoFi’s net interest up 477% year over year.

The company also gets a B grade in Louis’ Portfolio Grader, ranking the company above traditional banks, from C-grade Bank of America (NYSE:BAC) to D-grade Citigroup (NYSE:C).

To see more how Louis uses his AI-powered Portfolio Grader to the right time to buy the best blue chips, click here.

4. Freeport-McMoRan (FCX)

At first glance, shares of Freeport-McMoRan (NYSE:FCX) look unexciting at best. The world’s largest copper miner will generate only $1.55 earnings per share this year, a 35% decline from 2022. Falling copper prices and sagging Chinese demand have pushed share prices under $40.

But Eric sees significant opportunities for this blue-chip miner. This week at InvestorPlace.com, he notes how Freeport is quickly becoming a top user of artificial intelligence:

The terms “copper miner” and “artificial intelligence” do not obviously relate to one another. But in the case of Freeport, they do.

Freeport has been using a machine-learning model at its Bagdad copper mine in Arizona to boost production. This model uses data from sensors around the mine to “tailor” the ore-processing method to each of the seven distinct types of ore that come from the mine.

Because of the company’s success with AI at Bagdad, it is rolling out the technology across several other mines and expects to increase its annual copper production by a hefty 5% “with very little capital investment.”

The company is also a beneficiary of the EV revolution. Each new plug-in vehicle uses roughly 4X more copper than gas-powered ones, and the International Copper Association estimates that EV demand will add 1 million tons of annual demand by 2027. Copper futures reflect this reality, with forward prices trading at a 20-year high relative to spot prices.

That means Freeport could return to 2021-level profits by 2025, sending shares well into the $50 range.

U.S. Bancorp (USB)

Finally, Tyrik Torres highlights U.S. Bancorp (NYSE:USB) this week at InvestorPlace.com as a top safe stock to buy the dip.

U.S. Bancorp has been one of the most consistent performers among U.S. banks, delivering superior profitability and efficiency ratios throughout the years. In the second quarter of 2023, the bank reported a net income of $1.5 billion.

While U.S. Bancorp’s shares are down 9.5% year-to-date, the stock remains undervalued. U.S. Bancorp is trading at around 9.3 times forward earnings. The bank also offers an attractive dividend yield of 4.87%.

Put another way, U.S. Bancorp is one of the most profitable regional banks in America.

The company generates 11% return on equity, and Wall Street analysts expect the firm to produce $6.8 billion in net income this year, a 3% increase from 2022.

The bank is also surprisingly safe, thanks to a focus on conservative underwriting and diversified business lines. Quarter net charge-offs peaked at 2.5% during the 2007-08 financial crisis, far lower than the 3%-plus rates that others saw. Meanwhile, the company’s highly efficient non-banking businesses bring in a steady stream of profits. Payment services alone accounts for over a quarter of corporate profits.

That makes U.S. Bancorp’s recent drawdown an attractive opportunity to buy the dip. Shares have not yet fully recovered from this year’s regional banking crisis, and shares trade at only 1.1X book value – a level that suggests at least a 20% near-term upside, relative to returns.

The 2023 Quality Discount

Ordinarily, nice things are expensive. People pay more for first-class flights… luxury cars… designer handbags… you name it.

But what if high-quality items suddenly became cheap?

We’d be lining out the door at the Porche dealership!

That exact opportunity is now happening in the U.S. stock market. High-quality firms like U.S. Bancorp are trading at near book value while lower-returning ones like Morgan Stanley (NYSE:MS) are going for a higher 1.4X multiple.

The story is the same no matter where you look. Earlier this week, Vietnamese electric vehicle startup VinFast Auto (NASDAQ:VFS) became worth more than Ford Motor (NYSE:F) and General Motors (NYSE:GM) combined, despite selling only 7,400 vehicles in 2022. MotorTrend called the VinFast VF8 a project that would take “cubic dollars to fix” after basic functions like climate control and parking brakes failed to work properly.

There’s no hold function, so you’d better keep Creep mode engaged so it’s always sending power to the motors. Disable Creep, and the car will roll away in gear.

Meanwhile, blue chips like Volkswagen (OTCMKTS:VWAGY) are selling for less than 4X forward earnings.

In a topsy-turvy market like this, it’s no wonder investors are taking profits in expensive companies and moving into far safer bets.

As of this writing, Tom Yeung held a LONG position in GM. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.