So far this year, AI stocks are all the rage, and major indices like the S&P 500 are hitting new highs. However, things have been playing out differently in the world of penny stocks. This in turn highlights the need to know which penny stocks to sell.

Although the market is a whole lot more “risk on” than it was during 2022 and most of 2023, speculative stocks in “penny stock territory” ($5 per share or less), outside of AI penny stocks, have not come back into vogue.

For some stocks in this category, this may work in your favor. There are plenty of undervalued names that could, in time, deliver strong returns, whether via company-specific catalysts, or simply just via price discovery.

Still, while there are some diamonds in the rough, there are plenty of situations where a low trading price is not indicative of good value or potential for a big payoff down the road.

That’s the situation at hand with these seven penny stocks to sell. Stay away from each one, even if it’s a long-shot “lottery ticket” type bet.

Canopy Growth (CGC)

Back in January, I discussed how regulatory uncertainty made cannabis stocks like Canopy Growth (NASDAQ:CGC) a bad bet for 2024.

However, that full legalization of marijuana on the U.S. Federal level remains (at best) years away is not the sole reason it’s best to stay away from this stock.

In fact, there’s a larger, more urgent reason you should sell/avoid CGC stock: dilution risk. While Canopy raised $35 million two months back through a private placement, this likely did not mark the end of its capital raising efforts.

Mainly, due to persistent losses/cash burn, as seen most recently in last quarter’s financial results. Shareholder dilution played a big role in the stock’s 99.32% drop over the past five years. Another big slide may occur, if the share count rises but operating performance fails to improve.

Fisker (FSR)

Fisker (NYSE:FSR) first fell into “penny stock territory” last fall. Since then, it’s clearly been one of the top penny stocks to sell, with shares in the electric vehicle startup being in freefall mode, with FSR at one point falling to as low as 38 cents per share.

Still, some contrarians may want to believe that FSR stock is priced in a “heads I win big, tails I lose a little” type of situation. Unfortunately, there are not many signs pointing to this being the case.

With the company itself now doubting its chances of surviving as a going concern, Fisker’s survival may now hinge on whether Nissan (OTCMKTS:NSANY) proceeds with a deal to invest $400 million into the floundering EV company. This deal may help FSR avoid a total wipeout. However, the terms of the deal could limit upside for those buying into the stock today.

MicroVision (MVIS)

Last June, it may have seemed as MicroVision (NASDAQ:MVIS) was kicking off a “meme stock” revival, but this wave of speculative frenzy proved was short-lived. Since then, shares in this developer of lidar technology for self-driving vehicles has coughed back these gains and then some.

Although MVIS stock has yet to fall back to pre-meme prices, I wouldn’t rule that out as a possibility. While the company touted its latest lidar development progress in the latest quarterly earnings release, MicroVision clearly remains years away from commercializing and monetizing it.

The current EV sector slowdown leaves the market hesitant to invest in shares in EV and EV-adjacent companies. Barring the announcement of a partnership with an auto manufacturer, or an overall comeback in bullish sentiment for EV stocks, weak operating results and an uncertain future leave MVIS vulnerable to a continued drop in price.

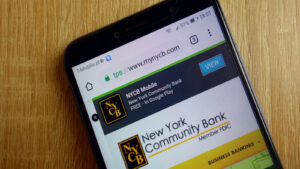

New York Community Bancorp (NYCB)

Since surprising investors with a surprise increase to its loan loss provisions, along with a dividend cut in late January, New York Community Bancorp (NYSE:NYCB) has gone from one of the highest-yielding and most undervalued bank stocks, to becoming one of the top penny stocks to sell.

NYCB stock has continued to tumble. Subsequent news, including further accounting write-downs and a CEO change, has kept raising concerns about the regional bank’s future prospects. The latest news calls into question the merits of making a high-risk, high potential return bet on NYCB, as it hits new all-time lows.

Even if New York Community Bancorp avoids a full-on failure, possible remedies to avoid one, like brokered deposits, or even the raising of additional equity, may negatively affect future results/share price performance. As the dust has yet to settle, err on the side of caution, and avoid/sell NYCB.

Office Properties Income Trust (OPI)

As its corporate name may suggest, Office Properties Income Trust (NASDAQ:OPI) is a real estate investment trust, specializing in the ownership of office properties. Admittedly, not only does OPI trade at a low stock price.

On a screener, OPI stock appears very cheap. This REIT sells for a tenth of book value. OPI’s price to funds from operations ratio is 0.82. That’s substantially below even the depressed valuations of other office REITs. Yet while cheap on a screener, take a closer look.

Upon closer inspection, it’s evident why OPI currently trades at such fire-sale prices. As I argued back in January, Office properties Income Trust faces a massive wave of lease expirations over the next two years. As office vacancy rates keep trending higher because of the shift towards a hybrid/remote workplace, finding new tenants could prove difficult.

Plug Power (PLUG)

I know what you’re thinking. Things are getting better for Plug Power (NASDAQ:PLUG), so is it one of the penny stocks to sell? Yes, as InvestorPlace’s Dana Blakenhorn recently pointed out, “going concern” risks have faded for this hydrogen energy company.

However, as Blakenhorn pointed out, this alone will not spark a comeback for PLUG stock. Don’t count on renewed enthusiasm for “green wave” stock to do the trick, either. The key to moving Plug Power in the right direction is improved fiscal results.

Unfortunately, this doesn’t appear on the immediate horizon. Even as the company touts that a major jump in “green hydrogen” demand could arrive starting late next year, this company has a long history of over-promising and under delivering. The market will probably continue to take a “show me” stance with PLUG. Hence, so should you.

Virgin Galactic (SPCE)

Virgin Galactic (NYSE:SPCE) went “to the moon” during the height of the special purpose acquisition company (or SPAC) bubble of 2020 and 2021.

However, shares in this early-stage space tourism company were buried by the “SPAC wipeout” that followed the boom, and have continued to trend lower.

This should come as little surprise, and not just because speculative growth stocks (outside of AI) have yet to come back in vogue. In recent months, there’s been plenty of negative news regarding SPCE stock. For instance, back in December, founder Richard Branson has announced that he doesn’t plan to make any future investments in the company.

More recently, an incident on one of its flights, plus the market’s response to Virgin Galactic’s latest quarterly results, have also weighed on SPCE. With commercialization happening slower-than-expected, as high cash burn persists, investors may continue to push shares down to even more discounted valuation.

On the date of publication, Thomas Niel did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.