The Fed leaves the target rate unchanged … we’re still on for three rate cuts in 2024 … the market celebrates with all-time highs … some sobering data about the U.S. consumer

Today, the Federal Reserve held rates steady at the current target rate of 5.25% – 5.50%. This was widely expected.

The question mark was the potential for a recalibration of the Fed’s Dot Plot. The fear was that the recent uptick in inflation might cause the Fed to lower its projected number of interest rate cuts in 2024, which could have roiled the markets.

Fortunately, that didn’t happen. Today’s updated Dot Plot continues to show three quarter-point interest rate cuts coming in 2024.

In response, stocks celebrated. The S&P topped the 5,200 level for the first time ever, the Dow hit its own record high, and the Nasdaq jumped 1.2% for another record close.

Let’s back up and fill in a few details to make sure we’re all on the same page

The Dot Plot is a graphical representation reflecting each committee member’s anonymous projection of where they believe rates will be at specific dates in the future. The Fed members update the Dot Plot once every three months.

In the December FOMC meeting, the Dot Plot showed a median forecast of three quarter-point rate cuts in 2024.

These cuts have been central to the bull market thesis in 2024. Historically, stocks outperform in a rate-cutting environment (unless the rate cuts are required to resuscitate a flatlining economy, which is not our case today).

But as noted a moment ago, the big question coming into today was whether the recent uptick in inflation (seen in January’s and February’s data) had spooked Powell and company, resulting in a lowering of rate-cut projections.

It hasn’t.

In addition to keeping three rate cuts penciled into the 2024 Dot Plot, here’s Powell from his live press conference:

I think [the hotter inflation data] haven’t really changed the overall story, which is that of inflation moving down gradually on a sometimes bumpy road toward 2%.

We’re not going to overreact to these two months of data, nor are we going to ignore them.

In another win for the bulls, Powell gave a hat-tip to a reduction in the pace of the Fed’s balance sheet runoff. Though he didn’t detail specifics, he noted a slowdown could be coming “soon.”

Back to Powell:

The general sense of the committee is that it will be appropriate to slow the pace of run-off fairly soon, consistent with the plans we’ve previously issued.

Finally, when asked if a strong labor market would be a reason not to cut interest rates, Powell said “no”:

In and of itself, strong job growth is not a reason for us to be concerned about inflation. No, not all by itself.

All-in-all, Powell gave the market what it wanted to hear, and stocks rallied in response.

The bull market is a “go” for now.

We’re pleased the Fed didn’t lower its rate-cut forecasts, and we’re hoping meaningful rate cuts arrive in time to help the U.S. consumer

Based on today’s updated Dot Plot, the majority odds are that the Fed will enact its first rate cut in June.

Frankly, it can’t come soon enough for the U.S. consumer who – though resilient – is showing widening cracks.

Now, we’re not going to make the case that the U.S. consumer is about to roll over because, frankly, we’ve made that mistake before. The much-referenced strength of the U.S. consumer has surprised us repeatedly.

But as we celebrate today’s record highs in the stock markets, let’s be open-eyed about some troubling data related to the U.S. consumer, which illustrates why we welcome the idea of a June rate cut.

We’ll begin with retail spending – the lifeblood of the U.S. economy.

Here’s Financial Times:

Evidence is mounting that many Americans have reached their limit for tolerating higher prices, raising questions about how much consumer expenditures will continue to power US economic growth this year.

After spending freely with savings built up during the coronavirus pandemic and income fueled by a healthy job market, consumers are becoming more cautious, according to comments from retail and consumer goods executives and official data.

Retail sales increased 0.6 per cent in February from the previous month, missing expectations by economists for a 0.8 per cent gain, according to Census Bureau data released this week. The increase reversed a 1.1 per cent decline from December to January.

“We did not begin the year with healthy robust consumer spending that we had at the end of last year,” said Steve Ricchiuto, chief economist at Mizuho Securities. “The economy is losing some momentum.”

Below, we get a visual on this waning momentum. We’re looking at a chart of Retail Sales from the Federal Reserve beginning in January 2010.

I’ve added a red line showing how retail sales have now stalled out for more than one year. And they’ve barely increased going back to April of 2022.

Now, let’s highlight an inconsistency…

FactSet reports that analysts forecast earnings growth rates (year-over-year) of 9.1%, 8.3%, and 17.3% for Q2, Q3, and Q4, respectively. And for all 2024, they expect earnings growth of 11.0%.

If retail sales are flatlining, and the U.S. consumer makes up 70% of our economy, these robust earnings growth rate estimates are in question.

But look again at the above chart…

There are stretches of mostly sideways movement that didn’t correspond with a recession. So, can we just ignore this slowdown in spending, or are there other data that give us pause about consumer health?

Additional signs of a tiring U.S. consumer

If U.S. consumers are healthy, then, presumably, they’d pay off their credit card balances each month.

After all, the average annual percentage rate (APR) for credit cards where the user has a balance is an eye-watering 22.75%. No one would choose to carry a balance and pay this interest rate.

Well, here’s USA Today:

Roughly half of all credit card holders now carry balances from month to month, Bankrate found in another survey, up from 39% in 2021.

The average borrower holds $6,360 in card debt, TransUnion reports, an all-time high…

More than one-third of American adults – 36% – have more credit card debt than emergency savings, according to an annual survey by Bankrate, the personal finance site. In more than a decade of polling, the figure has never been higher.

Meanwhile, we are seeing a growing number of credit card defaults.

Below is a post on X from the research shop Game of Trades. It shows how credit card default rates for small lenders just hit a new record high. We’re at levels not seen since 1991.

I’ll add that the personal savings rate clocked in at 3.8% in January.

That’s not an all-time low, but it’s in the arena. For most of the last decade, the savings rate has been above 5%.

There’s more trouble when we look at retirement accounts

Let’s jump to The Wall Street Journal from earlier this month:

A record share of 401(k) account holders took early withdrawals from their accounts last year for financial emergencies, according to internal data from Vanguard Group.

Overall, 3.6% of its plan participants did so last year, up from 2.8% in 2022 and a prepandemic average of about 2%…

Emergency distributions hit back-to-back record highs in 2022 and 2023, according to Vanguard, which administers 401(k)-type accounts for nearly five million people and published the data ahead of an annual report scheduled for June…

Nearly 40% of those who took a hardship distribution last year did so to avoid foreclosure, compared with 36% in 2022.

The reports keep coming…

On Tuesday, we learned that a recent study from Bankrate finds that 56% of Americans don’t have the savings to absorb a $1,000 emergency expense. Instead, they would put it on a credit card or get a loan from family or friends.

From Bankrate senior economic analyst Mark Hamrick:

The reality is that we are, unfortunately, essentially living in a paycheck-to-paycheck nation…

It’s quite remarkable in the current environment that even with low unemployment and a job market that has been both robust and resilient in recent years, that we still have this remarkably low percentage of Americans who could pay this emergency expense.

We agree. Unfortunately, history shows that we’re not going to enjoy this low unemployment rate forever.

Finally, it’s not just U.S. consumers who are struggling

Today, companies around the world are getting hit two ways: higher costs on their debt service, which eats away at their bottom lines; and less revenue based on the strained consumer we just looked at.

But you’re likely aware that we’re wrapping up an earnings season that has been much stronger than expected. So, where’s the evidence that companies are beginning to struggle?

Well, first, it’s not so much today’s absolute number, but rather, it’s today’s trajectory. We’re always trying to look at what’s coming tomorrow based on momentum today.

Here’s MarketWatch:

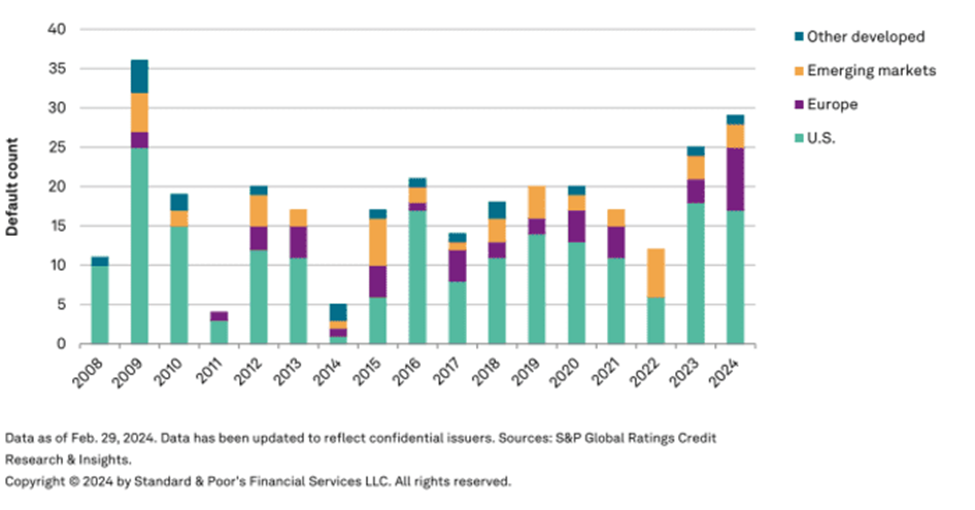

Companies around the world are defaulting on their debt at the fastest pace since the global financial crisis as high interest rates and stubborn inflation continue to take their toll, according to a report from S&P Global Ratings.

According to S&P, the number of corporate defaults has climbed to 29 since the start of the year, the highest tally at this point in a year since 2009.

While the majority of defaults occurred in the U.S., an uptick in European bankruptcies is alarming analysts.

So, what do we do with all this?

Well, first, we breathe a sigh of relief that the Fed is still on track for three rate cuts this year. Had we not gotten that, we’d be reporting on a very different market reaction today.

Then, we breathe a second sigh of relief that the end of peak target rates is in sight. As noted earlier, historically, stocks perform strongly in a rate-cutting environment.

But let’s remember that a quarter point cut in June won’t remove all financial stress weighing on the U.S. consumer and struggling companies.

So, wisdom suggests we look for opportunities to profit from what could be a robust continuation of this bull market. But at the same time, we make sure we’re invested in high-conviction stocks… we update our trailing stop-loss levels… and we trim down any position sizes that would do too much damage to our portfolios if they suffered a substantial drawdown…

But with those precautionary steps in place, we stay in the market.

Yes, the U.S. consumer is struggling, but we don’t know when the “uncle” point will come. In the meantime, stocks could have plenty more firepower in them.

Let’s take advantage while we can.

Have a good evening,

Jeff Remsburg