The current market rally has been very disproportionate and has been dominated by Big Tech. Many top technology companies with the largest market capitalizations have made significant rebounds since mid-2022. Many other businesses have recovered as well, but some have been stuck at bargain-basement levels for months. I believe scooping up such discounted stocks could lead to triple-digit returns in the coming years as they inevitably recover.

You can never go wrong by buying a profitable business with solid staying power. Such companies may have near-term problems right now. However, time and time again, companies with good margins have proven that the dips are only buying opportunities.

Here are seven such deeply discounted stocks to look into right now.

PayPal (PYPL)

PayPal (NASDAQ:PYPL) is a leading digital payments platform that enables online money transfers. The stock is trading at a steep discount compared to its pre-COVID highs, down nearly 50% from those levels. However, I believe PayPal’s core business remains robust despite the bearish sentiment we’re seeing in the broader fintech sector.

One key metric to watch is active user growth, which turned positive on a quarterly basis. This is crucial because PayPal’s monetization per user continues to improve. Declining active users has been the main reason why the company has been beaten down so much. So with that metric improving, I expect the stock to make a drastic turnaround.

The company delivered 10% currency-neutral revenue growth on $404 billion in total payment volume in Q1. Analysts expect 8% annual top-line growth going forward.

Meanwhile, PayPal is a cash-generating machine that is aggressively repurchasing shares. In Q1, the company grew non-GAAP earnings per share by an impressive 27% year-over-year.

I believe PayPal is poised for a sharp recovery in the coming quarters as market sentiment turns positive.

CVS Health (CVS)

CVS Health Corporation (NYSE:CVS) operates as a diversified healthcare company in the United States. The company’s stock price has plunged by nearly 30% since the start of April after the company reported disappointing Q1 results, with $1.31 of earnings per share missing estimates by 39 cents and revenue of $88.4 billion falling short by $767 million.

However, I believe this steep pullback presents a compelling buying opportunity for long-term investors. CVS stock is now trading at trough valuations not seen since mid-2019, despite the underlying business remaining fundamentally solid.

While the company is facing near-term pressures in its Medicare Advantage segment due to elevated utilization trends, management is swiftly implementing corrective actions to realign costs and optimize operations. CVS has a proven track record of successfully navigating industry challenges, and I’m confident the company will demonstrate that resilience once again. If CVS manages to meet earnings expectations going forward, the stock could easily double.

Headwinds from insufficient Medicare Advantage reimbursement rates in 2025 will likely pressure the entire industry. However, CVS’s scale advantages and diversified business mix should help mitigate the impact better than those of smaller peers. Notably, this stock also provides a 4.75% dividend yield.

Newell Brands (NWL)

Newell Brands (NASDAQ:NWL) manufactures and markets a wide range of consumer products. The company’s first-quarter results showed signs of a turnaround gaining traction, with core sales declining just 4.7% compared to 9.3% in the prior quarter. NWL stock has plummeted 86% from its 2017 peak. However, I believe it is now bottoming out, offering a compelling entry point with limited downside risk at these levels.

The company has new products like Sharpie Creative Markers and Paper Mate InkJoy Gel Bright Pens, which should see consistent growth. Despite the challenging environment, Newell’s revenue has remained relatively resilient, and analysts project earnings growth of around 15-20% annually going forward.

While rising interest costs are currently pressuring profits, I expect future rate cuts to provide a significant earnings boost as net interest loss narrows.

Newell is already profitable, which I believe makes it quite low-risk at current levels. As the turnaround initiatives take hold and the macro backdrop improves, I see a path for the stock to potentially double or more from these depressed levels. You can also sit on its 3.75% dividend yield as it recovers.

Estee Lauder (EL)

Estee Lauder (NYSE:EL) is a global leader in prestige beauty. The company’s stock has been battered, plummeting nearly 70% from its peak as the post-pandemic discretionary spending bubble burst. With consumers feeling the pinch, it’s no surprise Estee Lauder’s sales have taken a hit.

However, I believe now could be an opportune time to scoop up shares before an inevitable rebound. The company’s FY24 Q3 results showed encouraging signs, with organic sales growth of 6% exceeding expectations. Management also made significant progress in reducing inventory pressures and realizing strategic pricing.

Estee Lauder is poised for an inflection point in the second half of fiscal 2024. The company expects accelerating sales momentum and expanding operating margins. Plus, its $1.1-$1.4 billion profit recovery plan should boost earnings significantly over time.

I’m confident Estee Lauder’s iconic brand portfolio and loyal customer base will power a resurgence once rate cuts revive discretionary spending.

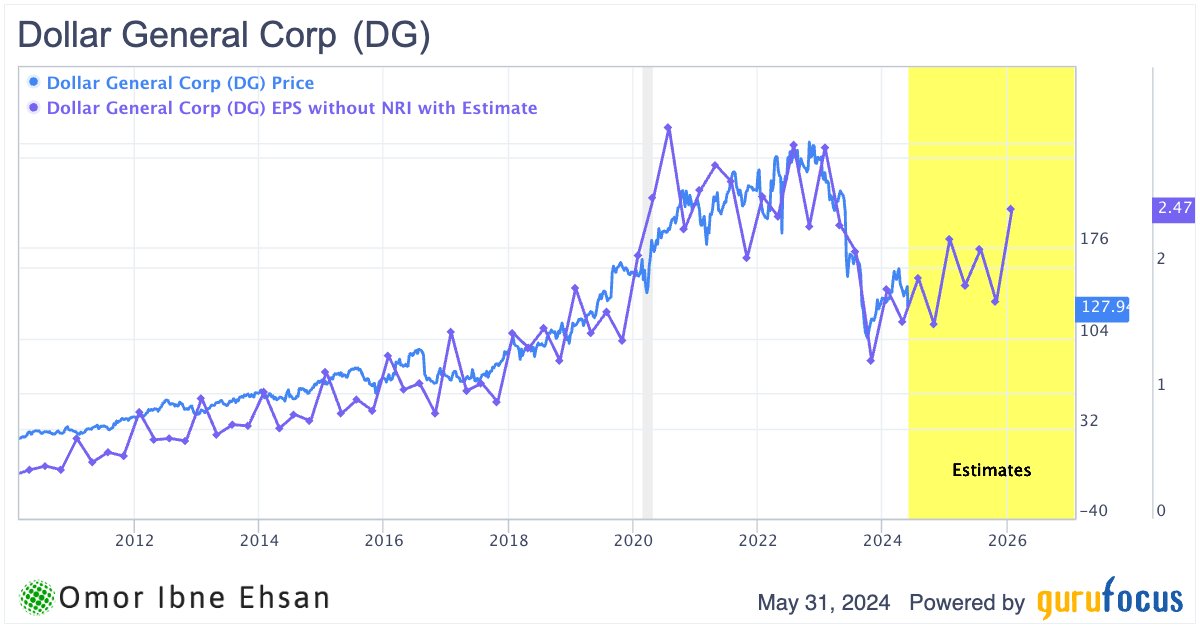

Dollar General (DG)

Dollar General (NYSE:DG) operates a chain of discount retail stores across the United States. Despite a recent earnings stumble and share price decline, I remain bullish on DG stock for the long haul. Much like Estee Lauder, an earnings recovery here should drive the stock higher over the coming quarters.

In Q1, net sales grew 6.1% to $9.9 billion, while same-store sales rose 2.4%, driven by over 4% traffic growth. Management highlighted accelerating market share gains in consumables and non-consumables. However, softness in discretionary categories due to consumer pressures weighed on results.

While concerning, I believe these near-term headwinds are more than priced in after the stock’s steep correction. At these levels, DG stock is simply too cheap for a best-in-class retailer. The company’s unrivaled footprint positions it to thrive long-term. GuruFocus’ price model also agrees with my view:

I expect Dollar General to handsomely reward patient investors over the long-term. Don’t be surprised to see this stock deliver triple-digit returns in the coming years as short-term pressures abate. This stock also gives investors a modest 1.84% dividend yield.

Southwest Airlines (LUV)

Southwest Airlines (NYSE:LUV) operates as a passenger airline in the United States. The company’s stock has been crushed, down nearly 54% from pre-pandemic levels, as it took on significant debt during the pandemic that became much more expensive to service after aggressive rate hikes. The biggest problem here is actually Boeing (NYSE:BA), in my opinion. However, I expect Boeing to fix its delivery and safety problems after the backlash.

While Southwest achieved record Q1 operating revenues and passengers, its negative earnings per share of -36 cents missed estimates by 2 cents. Management is rightly disappointed with this performance. To improve profitability, Southwest is optimizing its network by eliminating service to four cities, reducing flights in Atlanta and Chicago, and adjusting capacity on certain days.

I believe these moves, combined with the likelihood of Fed rate cuts ahead, could be the catalyst to send this beaten-down stock soaring. If Boeing regains its footing, this could also help significantly. Yes, Southwest faces challenges, but it has solid staying power. Its fleet has also started to grow again.

Trading at such a steep discount to pre-pandemic prices, I see the potential for LUV stock to double or more for patient investors willing to ride out this turbulence. This stock has a 2.86% dividend yield to sweeten the deal.

Five Below (FIVE)

Five Below (NASDAQ:FIVE) is a leading high-growth value retailer offering trend-right products to tweens and teens. Thanks to several powerful megatrends aligning in its favor, I believe this beaten-down stock has significant recovery potential.

Management’s long-term goal of 3,500+ stores by 2030 looks achievable, given the record 205 new locations opened in 2023 alone. Five Below’s unique “Five Beyond” store-within-a-store format, now in over 50% of locations, clearly resonates with the target demographic. Comparable sales rose 3.1% in Q4 2023, driven by these converted stores.

The value-focused Gen-Z consumer should increasingly flock to Five Below’s extreme value proposition in the years ahead, especially if macroeconomic pressures persist. Five Below is also ideally positioned to capitalize on the accelerating trends of Y2K and 90s nostalgia.

At a mere 10-times forward earnings, this proven retail growth story looks far too cheap if management can execute. Analysts also seem very bullish, and it’s hard to disagree.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.