When the dust settled after Monday’s trading session, shares of doughnut retailer and wholesaler Krispy Kreme (NASDAQ:DNUT) found themselves up more than 6%. Driving the positive sentiment was the company’s partnership with McDonald’s (NYSE:MCD). The deal could potentially expand DNUT’s total addressable market. However, the bears don’t see it that way, presenting a compelling contrarian trade for DNUT stock.

Krispy Kreme saw investor enthusiasm amid rising expectations for its upcoming deal with the fast-food giant. Under the agreement, Krispy Kreme doughnuts will be sold at thousands of locations under the Golden Arches brand. For Krispy Kreme, it will open a whole new avenue within the fast-casual eatery space. It also benefits McDonald’s, especially as it adds value to its breakfast menu.

Notably, analyst Bill Chappell raised his price target for DNUT stock to $15 from $13. Chappell believes that the partnership will “accelerate revenue growth” for Krispy Kreme. However, many traders don’t feel the same way.

Unusual Options Activity Underlines Bearish Sentiment

Following the close of the June 10 session, DNUT stock ranked among the top names in terms of unusual stock options volume. This data focuses on the difference between current volume and the average volume over the trailing month. Primarily, it enables retail investors to better understand what the smart money may be putting its funds into.

In the case of DNUT stock options, total volume reached 10,564 contracts against an open interest reading of 48,694 contracts. The difference between Monday’s session volume and its 30-day average came out to nearly 232%. Notably, call volume outweighed put volume by a ratio of almost 40 to 1.

At first glance, such a ratio favoring calls seems strongly bullish. However, calls can be sold, which may have negative implications. Indeed, DNUT’s options flow screener – which focuses exclusively on big block transactions likely placed by institutional investors – shows that net trade sentiment landed at $169,000 below breakeven, thus favoring the bears.

Among options with bearish sentiment, the biggest premium came out to $116,100. This was for the 2025 Jan. 17 $10 (sold) call. In contrast, among options with bullish sentiment, the biggest premium reached only $11,400.

However, with Krispy Kreme beating its consensus revenue target in the first quarter, there’s reasonable hope that the company can match analysts’ view for fiscal 2024 sales, which stands at $1.79 billion. If so, assuming a shares outstanding count of 168.73 million, DNUT stock would be trading at 1.07x projected sales.

That’s pretty close to the restaurant sector’s average sales multiple of 0.99x. Given the brand power and compelling McDonald’s deal, DNUT stock could be relatively undervalued.

Trade of the Day: Buy DNUT Stock Against Bearish Pressure

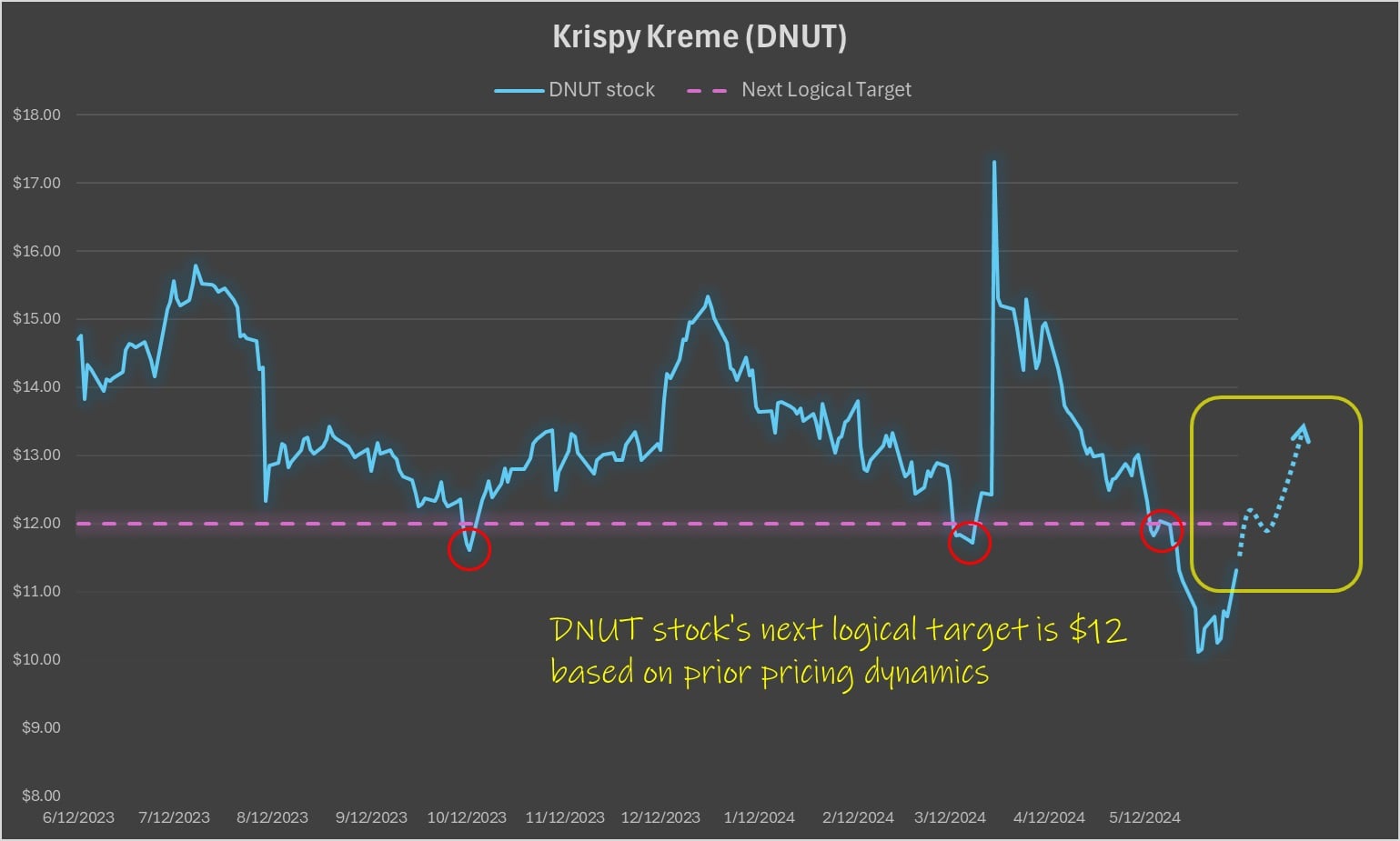

Due to the underappreciated value tied to DNUT stock, I’m more inclined to be a buyer rather than a seller. For those who want to take the risk, the next logical target would be the $12 price point.

Throughout the past 52 weeks, there have been three pronounced efforts to drive DNUT stock below this threshold. One attempt occurred in October and the other occurred in March. The third attempt last month was ultimately successful.

Thus, for the bulls to regain credibility, they must drive Krispy Kreme’s per-share price above the $12 price point. Notably, among Wall Street analysts, DNUT stock enjoys a unanimous strong buy rating with an average price target of $20. So, $12 is a very conservative target.

For those who really want to ramp up their risk-reward profile, the 2025 Jan. 17 $12.50 call could be enticing because it affords plenty of time for the analyst view to come right. If DNUT stock reaches $20 sooner than Jan. 17 of next year, the profit could be enormous.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.