What Buffett’s move into cash means … should you be overweight cash? … lump-sum investing vs. dollar cost averaging … how Eric Fry is sizing up AI investing today

If Buffett is moving into cash, then I am too.

That was the takeaway from a friend as we discussed the stock market yesterday.

His argument was rooted in logic, punctuated by various “Buffettisms.”

For example, to support his point, he referenced Buffett’s popular quote, “be fearful when others are greedy and greedy when others are fearful.” His logic was that with the market near all-time highs today, people are greedy.

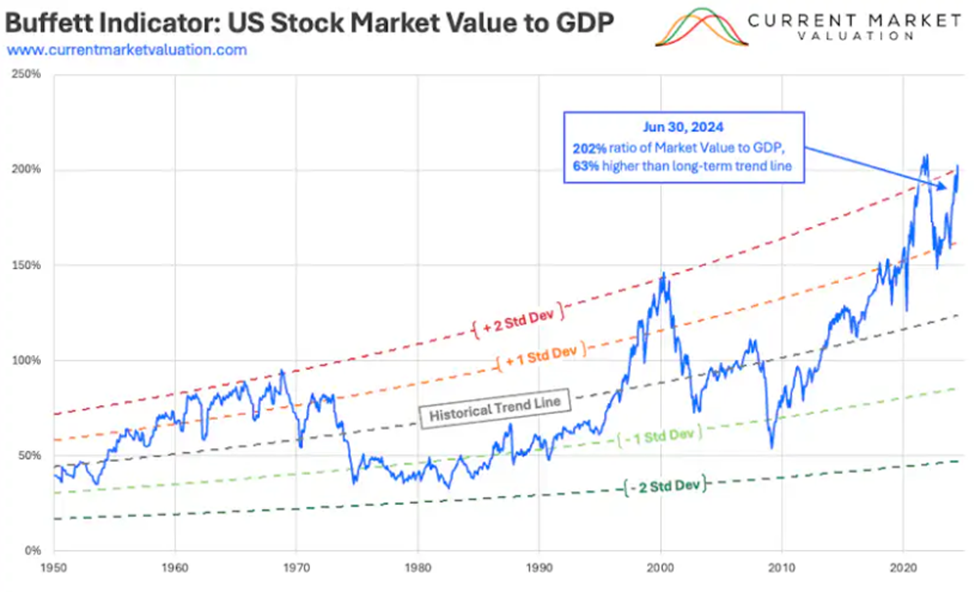

He also pointed toward the “Buffett Indicator” which is the ratio of the total U.S. stock market to U.S. GDP. Today, it suggests that stocks are incredibly expensive.

By the way, he’s not wrong about that. Below, you can see that, as of June 30, the Buffett Indicator clocked in at 202%, which gives it a “strongly overvalued” reading of two standard deviations above average.

My friend also cited Buffett’s recent sale of Apple, a recent article suggesting Buffett is preparing for a higher corporate tax rate from Kamala Harris (he believes she’ll win), the factoid that Buffett now owns more treasuries than the Federal Reserve, and then the overall market that now trades just beneath all-time highs.

Put it altogether, and the takeaway for my friend was simple: go overweight cash…by a lot.

Is such a move the right call for you today?

After all, if this market is so unattractive to Buffett that he now holds the most cash in the history of Berkshire Hathaway, should you and I follow suit?

Well, to begin our analysis, let’s start with an important question…

Are you running a multi-billion-dollar portfolio?

Buffett is a victim of his own success.

When you make as much money as he has over the decades, your portfolio grows so enormous that it limits your universe of potential investments. But with a smaller portfolio size, the world is your oyster.

Let’s rewind to this gem from Buffett back in 1999:

The highest rates of return I’ve ever achieved were in the 1950s. I killed the Dow. You ought to see the numbers. But I was investing peanuts then.

It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that.

One reason why Buffett is so heavily in cash today is because there aren’t as many great investment options in his weight class.

Analyst John Huber recently ran the numbers on what this means. From MarketWatch:

Buffett is running a roughly $600 billion portfolio. Working backwards, there are only 27 U.S. stocks that are $300 billion in market cap, where a 10% position in the company, and 5% of the Berkshire Hathaway portfolio, would be $30 billion. Expanding his pool of stocks overseas, there’s another 100 he could even look at, says Huber.

“The incredible size of the portfolio, plus the high valuations in large cap stocks, makes it almost impossible to put cash to work at the rates of return he’d like (double digits),” says Huber. “It’s not market timing, it’s just a product of valuation levels and a very tiny opportunity set that shrinks each year.”

That’s a key line – “it’s not market timing.”

I’m reasonably sure that if Buffett was running just $1 million today, he’d be fully invested or close to it, and he certainly wouldn’t be lamenting a lack of investment opportunities.

But what about the high yields in savings accounts today and the risk of a market crash?

High-yield cash accounts can feel safe. And in the short-term, they are. But parking too much of your net worth in cash, for too long, is an awful idea.

Sure, you’ll sidestep a potential market crash…but the opportunity cost is likely to be worse than the crash itself.

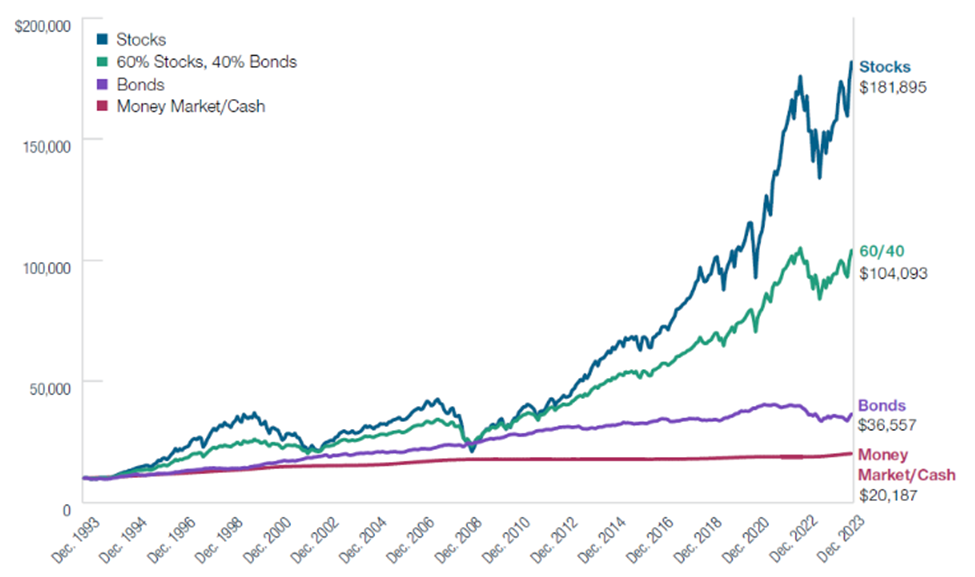

To illustrate, below is data from T. Rowe Price that compares returns from stocks, a 60/40 portfolio, bonds, and cash for the 30 years between 1993 and 2023.

Despite all the bear markets and corrections along the way, stocks returned about 18X while cash returned just 2X.

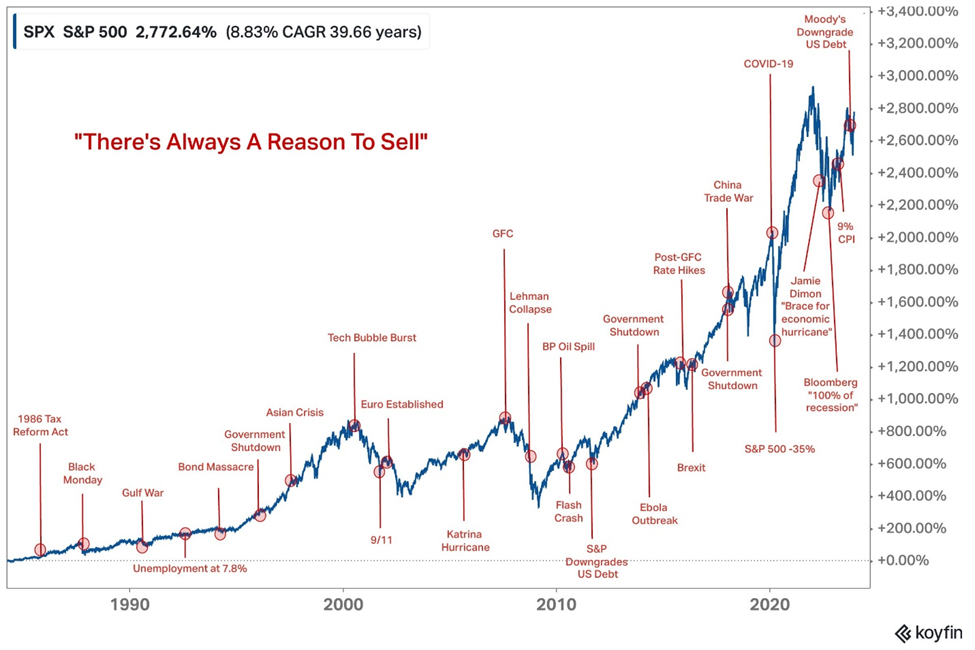

And if you’d like a stroll down memory lane for all the reasons there were to abandon stocks over this timeframe, enjoy the chart below.

Remember – getting out of the market is the easy part. Getting back in is where the challenge lies.

So, does this mean you should just find the best stocks you can, then cannonball in today?

Well, yes… (with some qualifications).

One of the great questions of investing is “do you go ‘all in’ with a big chunk of cash, or do you drip it in slowly.”

If we go by the numbers, the wisest plan is to put it all into the market right now – today – and be done with it.

Vanguard ran a study spanning from 1976 to 2022. It found that lump sum investing outperformed dollar cost averaging (DCA) 68% of the time after one year.

This advantage occurs because lump sum investing maximizes the time your money is in the market, allowing it to compound over a longer period.

Morgan Stanley ran a similar study, concluding that in more than 55% of cases, lump sum investing generated slightly higher annualized returns compared to DCA. And a study by Northwestern Mutual found that over a 10-year period, lump sum investing beat DCA about 75% of the time.

Now, while the statistics favor lump-sum investing, there’s a good reason why it terrifies so many investors…

When you choose lump-sum and get your timing wrong, it’s brutal.

This points us toward practical implementation strategies…

The longer your investment horizon, the more you should default to lump sum investing.

The shorter your investment horizon, the greater the likelihood that DCA might be a better fit – at least from a psychological perspective. It balances the “offensive” need to be invested with the “defensive” need to avoid a major portfolio drawdown that might impact your retirement or financial goals.

So, how long does your investment horizon need to be for the offensive firepower of lump sum investing to outweigh the defensive posturing of DCA?

There’s no perfect break-even point. But most studies suggest it’s in the three-to-five-year range.

One critical detail…

Regardless of whether your next allocation to stocks is a smaller DCA amount or a massive lump sum, commit to it. In other words, don’t do what I’m about to show you.

Below is the latest meme going around that illustrates how most investors handled the recent market volatility. The stock market line is a loose-yet-accurate proxy for what the S&P just did.

Take a moment and ask yourself a few questions today…

How exposed to the market are you today? Does your exposure level adequately reflect your investment horizon and/or your risk tolerance? Or are you potentially underinvested (or even overinvested)?

Circling back to my friend, I believe he’s basing his investment decisions on someone else’s market strategy. Unless his overweight cash position is well-timed and relatively short-lived, I’m afraid it’s likely to be counterproductive to his long-term goals.

Are you in danger of the same – whether you’re too conservative or too aggressive?

As investors, we need to do these occasional check-ins to safeguard against “emotional drift.” By that, I mean the tendency to let short-term emotions (fear or greed) result in a portfolio composition that no longer accurately reflects long-term goals.

So, where are you today?

Now, this doesn’t mean investors can ignore today’s valuations for specific stocks, even as we grow excited about various opportunities

On this note, let’s rewind to the Dot Com Boom in 1999/2000, and the valuation landscape at that time.

Here’s our macro expert Eric Fry:

In January 2000, investors knew that the internet would change the world. So, they bid up the market caps of the Top 5 tech stocks to record heights…

- Microsoft Corp. (MSFT) to $600 billion

- Cisco Systems Inc. (CSCO) to $316 billion

- Oracle Corp. (ORCL) to $308 billion

- Intel Corp. (INTC) to $275 billion

- IBM Corp. (IBM) to $188 billion

All of this felt perfectly reasonable at the time.

However, these companies couldn’t stay at those lofty valuations, and all but IBM declined over the next decade. In fact, Cisco and Intel still trade below their 2000 peaks.

The truth is that high share prices have a habit of robbing future investors of returns. If a stock rises 10% today, that usually means 10% less upside is available for tomorrow. And even the highest-growth companies can take decades to “fill out” inflated market valuations… if they ever do at all.

As Eric points out, valuation matters. A lot.

So, what does this mean for AI, today’s proxy for the internet boom in 2000?

If AI stocks are trading at horribly inflated valuations on par with the Dot Com peak, then a lump sum investment today might not be a great idea. DCA would seem wiser.

But perhaps there are smaller, more obscure AI plays trading at attractive valuations that will turn into tomorrow’s most explosive success stories. In that case, lump-sum investing appears to be a far-wiser choice than DCA.

Such questions bring us to Eric and his live event tomorrow, the Road to AGI Summit at 1 PM ET. You can automatically sign up by clicking here.

Eric will discuss what’s coming with AI itself – the technology and its capabilities. But then there’s the investment angle. And not just the obvious companies that you’re likely thinking of today (that might have loftier valuations). Eric has zeroed in on some alternative ideas, some with no visible ties to AI all (yet deserve your consideration). You’ll hear more tomorrow.

Plus, when you join the event, you’ll get Eric’s three-part “future-proof” blueprint, as well as a brand-new stock idea for The Road to AGI that he’ll give away for free.

We’re expecting a massive turn-out, and we’re getting down to the wire on sign-ups. So, to instantly reserve your seat, just click here.

Circling back to the top of today’s Digest…

Does your portfolio and market exposure today suggest that you’re properly positioned relative to your long-term goals? Or has a shorter-term, emotion-based influence begun to call the shots?

If it’s the latter, this is your wake-up call.

Remember what you want to accomplish through investing and make that your North Star.

After all, though “old Buffett” might be overweight cash today, I seriously doubt we’d find the same positioning from “young Buffett.”

Have a good evening,

Jeff Remsburg